7 Mistakes You're Making with Working Capital Loans (and How to Fix Them)

- Stuart Long

- Feb 20

- 5 min read

Working capital loans can be a lifeline for growing businesses, or a fast track to financial stress. The difference? Knowing what you're doing before you sign on the dotted line.

I've seen too many business owners rush into working capital financing without fully understanding the terms, costs, or whether it even makes sense for their situation. The result? Higher costs, cash flow crunches, and headaches that could have been avoided with a little homework upfront.

Let's walk through seven common mistakes business owners make with working capital loans, and more importantly, how to fix them before they derail your profitability.

Mistake #1: Focusing Only on the Loan Amount (Not the Total Cost)

Here's the thing: a $50,000 loan isn't really $50,000 if you're paying back $65,000.

Too many business owners get excited about approval amounts without calculating what they'll actually owe. Short-term loans, merchant cash advances, and alternative financing often come with factor rates, origination fees, and effective APRs that turn what looks like affordable capital into an expensive mistake.

How to fix it: Before you accept any offer, calculate the total repayment amount and the effective APR. Compare multiple lenders and financing products side by side. A slightly lower loan amount with better terms almost always beats a bigger loan with hidden costs.

Mistake #2: Borrowing More Than You Actually Need

It's tempting to take the maximum approved amount "just in case." After all, having extra cash on hand feels safer, right?

Wrong. Every dollar you borrow costs you money, whether you use it or not. Overestimating your funding needs creates unnecessary debt, shortens your cash runway, and puts extra strain on your monthly cash flow.

How to fix it: Build a simple cash flow projection before you apply. Know exactly how much you need, when you need it, and how you'll use it. If you're approved for $75,000 but only need $50,000 to cover inventory or bridge a seasonal gap, take the $50,000. Your future self will thank you when repayment starts.

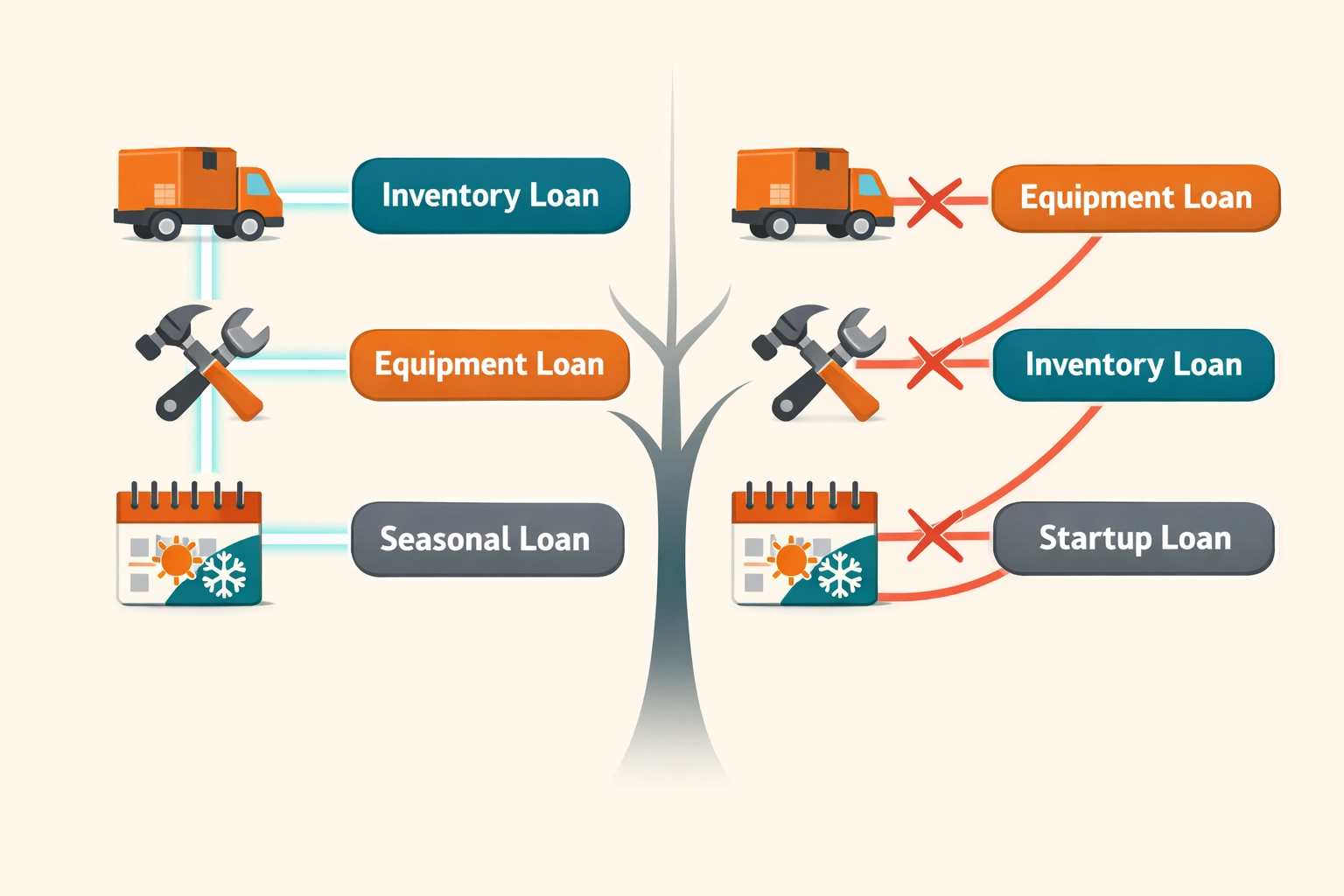

Mistake #3: Using the Wrong Type of Financing

Not all working capital loans are created equal. Using a merchant cash advance to buy equipment or a long-term loan for short-term cash flow gaps creates mismatched terms, inflated costs, and unnecessary repayment pressure.

For example, if you need quick cash to cover payroll for two months while waiting on receivables, a short-term working capital loan makes sense. But if you're financing a major equipment purchase or expansion, you need longer repayment terms, not daily ACH withdrawals.

How to fix it: Match the loan duration with your use case. Short-term needs deserve short-term solutions. Long-term investments require long-term financing. When in doubt, consult with a financial advisor who understands business financing structures. At STL Professional Services International, we help business owners evaluate financing options and choose the right product for their specific situation, not just what's easiest to get approved for.

Mistake #4: Ignoring Your Cash Flow Reality

This is the big one. Taking on loan payments you can't realistically afford is the fastest way to create a cash crisis.

If your revenue is declining, your bank account is frequently overdrawn, or your monthly cash flow swings wildly, adding a daily or weekly repayment obligation will only make things worse. Some business owners assume revenue will magically improve once they have access to capital, but that's wishful thinking, not a strategy.

How to fix it: Before applying, review your average monthly revenue and expenses over the last 6–12 months. Understand exactly what your repayment schedule will look like, daily ACH? Weekly payments? Monthly installments?, and make sure it fits comfortably within your existing cash flow. If the numbers are tight, don't force it. Instead, focus on improving collections, cutting costs, or exploring revenue-based financing that adjusts with your sales.

Mistake #5: Submitting Messy or Inaccurate Financial Documentation

Incomplete financials don't just slow down your approval, they can tank it entirely. Lenders need accurate bank statements, profit and loss reports, and balance sheets to evaluate your creditworthiness and repayment ability.

Submitting outdated bookkeeping, inconsistent bank statements, or missing documents signals disorganization and risk. And guess what? Risky borrowers get worse rates (or flat-out denials).

How to fix it: Keep your bookkeeping updated monthly or quarterly. Use accounting software like QuickBooks or Xero to stay organized. Before you apply for financing, review your financials with a critical eye. Better yet, work with a business consultant who can help you present clean, accurate documentation that strengthens your application and qualifies you for better terms.

STL Professional Services International specializes in helping businesses clean up their financials, build accurate cash flow forecasts, and position themselves for smarter funding decisions. When your numbers are tight, lenders notice, and reward you with better offers.

Mistake #6: Neglecting Your Accounts Receivable Collection Process

Here's a truth most business owners don't want to hear: If customers aren't paying you on time, you're essentially giving them an interest-free loan while you're paying interest on yours.

Slow accounts receivable collections are one of the biggest drains on working capital. When invoices sit unpaid for 60, 90, or 120+ days, you're forced to borrow more, and pay higher rates, to cover the gap.

How to fix it: Tighten up your collections process. Send invoices immediately, follow up consistently, and implement payment terms that incentivize early payment (like 2% net 10). Consider offering multiple payment options to make it easier for customers to pay quickly.

Treat your receivables like the critical asset they are, not a passive line item on your balance sheet. Faster collections mean less need for external financing, and when you do borrow, you'll qualify for better rates because your cash position is stronger.

Mistake #7: Not Shopping Around for Better Terms

Accepting the first loan offer you receive is like buying the first car you test drive. Sure, it might work: but you'll probably overpay.

Rates, fees, and terms vary wildly between lenders and products. A traditional bank, an online lender, and an alternative financing company could all offer working capital loans with completely different cost structures. Without comparing multiple offers, you have no idea if you're getting a fair deal.

How to fix it: Request quotes from at least three different lenders. Compare total repayment costs, not just interest rates. Pay attention to fees, prepayment penalties, and repayment flexibility.

If navigating multiple lenders feels overwhelming, work with a trusted advisor who can help you evaluate offers and negotiate better terms. At STL Professional Services International, we take the guesswork out of business financing by helping you compare options, understand the fine print, and choose solutions that actually support your profitability goals.

The Bottom Line

Working capital loans aren't inherently good or bad: they're tools. And like any tool, they work best when you know how to use them properly.

Avoid these seven mistakes, and you'll set yourself up for smarter borrowing, stronger cash flow, and better long-term profitability. Rush in without a plan, and you'll pay for it, literally.

If you're considering a working capital loan and want expert guidance on whether it's the right move (and which option makes the most sense for your business), let's talk. STL Professional Services International helps business owners make confident, data-driven financing decisions that fuel growth without sacrificing profitability.

Ready to avoid these costly mistakes? Reach out today, and let's build a smarter working capital strategy together.

Want a quick, high-value second opinion on your specific situation? Choose a paid option that fits what you need:

15-minute brief talk (quick clarity + next steps):https://calendly.com/stlpsi/15-minute-meeting

50-minute deeper dive (for a more in-depth review of your situation):https://calendly.com/stlpsi/50min-minute-meeting

Comments